Yellen model proves incredible inflation predictor

This is a follow up to the ‘Yellen model’ blog written in April 2021: US inflation to overshoot 2% consensus-view outlook to beyond 3

DM housing: Lots of monitoring, no real brakes

The restraint to the DM housing sector does not look as though it will come from financial policy (or a financial accident), but from (further) rising costs and prices eventually undermining affordability. The most that central banks are generally doing is ‘monitoring’ the situation. The much-asked question is whether (and

US inflation to overshoot 2% consensus-view outlook to beyond 3%

In 2022, the U.S. Fed forecasts inflation to fall back to 2%. But the inflation model developed by the then Fed Chair Yellen (who is the current Treasury Secretary) says otherwise. Her model uses slack (unemployment relative to NAIRU) import prices and expectations as its key drivers. Despite a widely

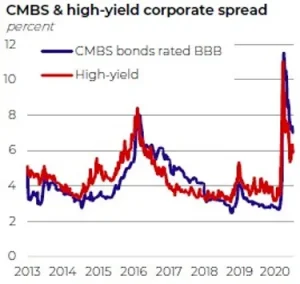

‘Whistling past the graveyard’: Archegos meltdown – yet another shockwave in the financial sector

Lending banks are often thought be the major holders of international exposure and therefore country risk. Non-bank financial institutions (NBFIs) — hedge funds, pension funds, private equity funds and others — often incur and accumulate significant country risk as well. Of timely importance, the recent failure of family office Archegos

Estimating Global Uncertainty? Better to consider source of uncertainty.

The level of global uncertainty should be considered, and perhaps it can be measured. The International Monetary Fund has quantified an answer: an uncertainty index. To develop an “uncertainty index”, the IMF ‘text mined’ through quarterly Economist Intelligence Unit country reports, reviewing editions from the 1950’s to date. They then

5 Lessons Learned for Banks Having Acquired an FI

5 lessons you need to know to smooth out model integration So, your bank has newly acquired a financial institution. But this may keep you up at night, fretting over how to integrate those models, but more so, how to communicate with the other firm about such. 1. Absolutely make

Banks struggling with Covid-era risk management as stat models only good as history

A huge struggle for banks with this ongoing pandemic. As you well know, statistical models are only good as the history: with sharp change (esp. unemployment rate), there is a disconnect in the model. So how does this bode for banks? Management overlay and qualitative adjustment abound. Colleagues at banks

Long run on surging house prices to come in the US and other DMs — macro-prudential brakes possible?

For in-depth analysis, see attached paper by Phil Suttle.

A possible shakeup in the US small bank landscape?

See attached research note, US Commercial Property Accidents Ahead, written by my colleague, Philip Suttle (brief bio below): Institute of International Finance, Chief Economist Barclays Investment Bank, Global Head of Emerging Market Research Federal Reserve Bank of New York The World Bank, Director, Development Finance Group JP Morgan, Economist Bank

Why the Art of Risk Management Prevails over the Science

EXPERIENCE AND THE HUMAN DIMENSION OF RISK One could reasonably ask why so much emphasis is placed on experience in risk estimation, modeling and management. While experience benefits people in any line of work, there is a good reason why the introduction of new technology, new sets of regulatory rules,